Everything written about managed accounts is for the investor. Not this.

Managers think they know what they're signing. Allocators think they know what they're buying. Both are usually wrong about the same thing.

Ten years ago, a manager offering you a managed account was telling you something. It usually meant they needed the assets badly enough to run your money on your terms, in your name. You didn’t want it. As one investor put it recently, a managed account was the last resort and you stayed away from the manager who was giving you one.

That signal has now flipped completely. The most sought-after single-PM talent in the market actively wants managed accounts, and it’s not because they have to take it. The structure that used to mark a manager as desperate now marks them as a serious entrepreneur who has left a pod to run their own book.

If you are an emerging manager, the question is no longer whether you’ll be asked about managed accounts but whether you understand what actually changes when you sign one, because almost everything written about this structure describes the benefits to the person on the other side of the table, the investor.

This is the piece I wish managers had in front of them before their first managed account conversation. It is equally useful if you sit on the investor side and are weighing whether to allocate this way. Most of what follows is the same set of facts read from two seats.

What a managed account actually is

Strip away the acronyms first. You might have heard it called any of these: separately managed account, an SMA, a segregated account, or a dedicated managed account on a platform. They may differ in the plumbing, but the core idea is identical.

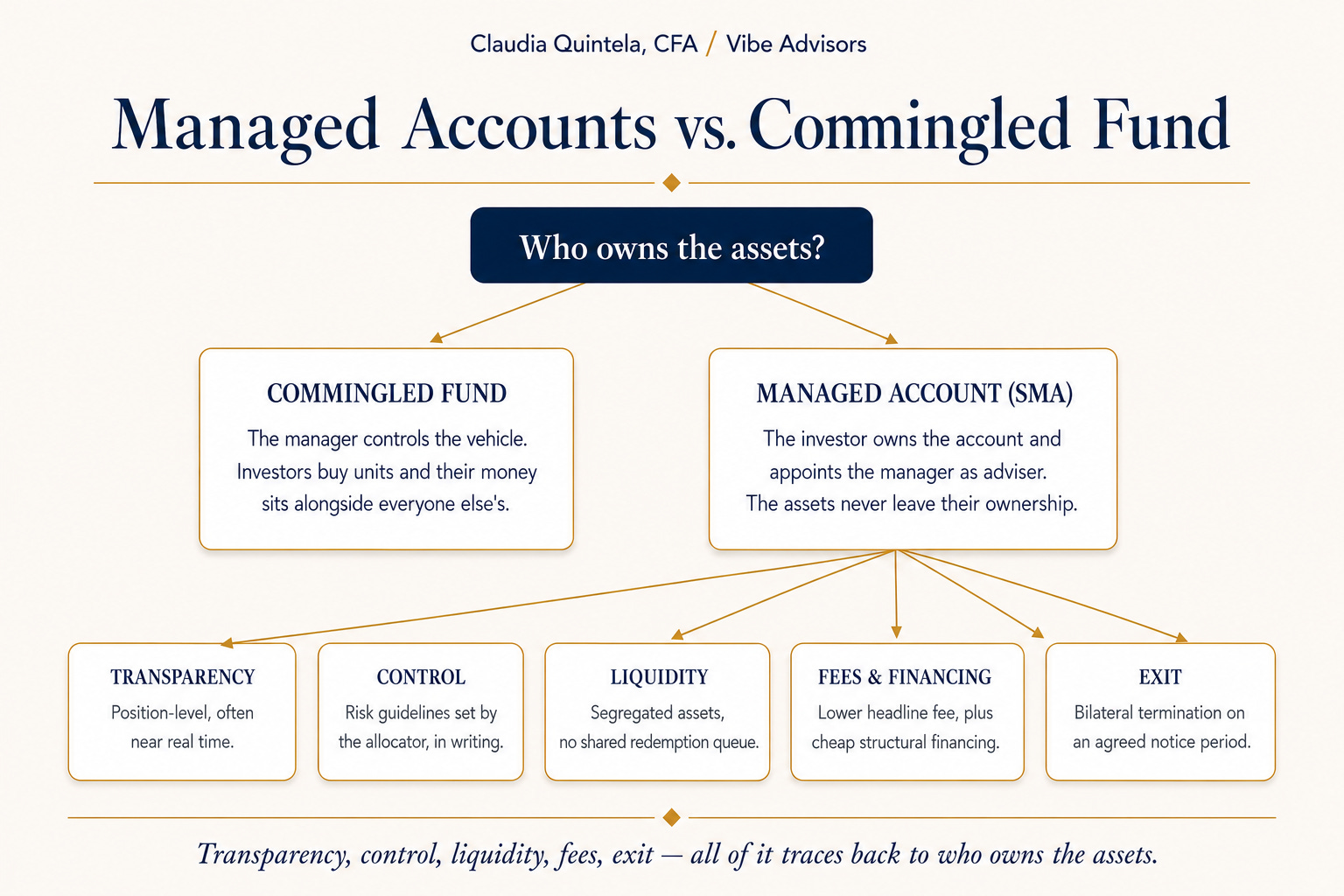

In a commingled fund, the manager controls the vehicle. Investors buy units. Their money sits alongside everyone else’s, and the manager decides, within the fund documents, what happens to it.

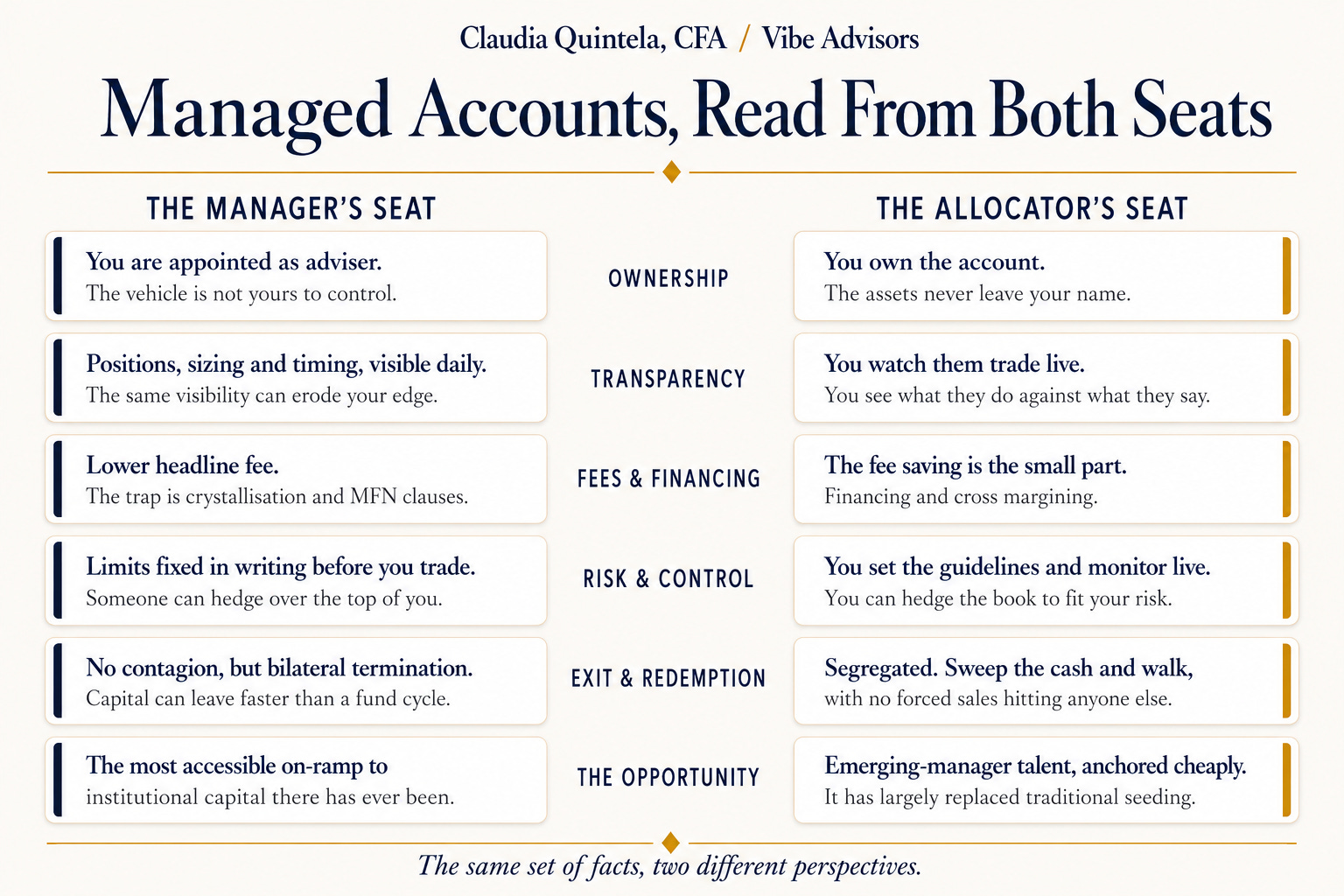

In a managed account, the investor owns the account. They appoint the manager as investment adviser and delegate trading authority. The assets never leave the investor’s ownership. That single distinction, who owns the assets, is where every other difference comes from. Transparency, control, liquidity, fees, the exit mechanics, all of it traces back to ownership sitting with the allocator rather than the manager.

KPMG framed the original driver years ago and it still holds. Demand for transparency, liquidity and asset segregation rose after 2008 and the fraud cases that followed. Institutional investors, now around two-thirds of total hedge fund assets, wanted control rather than a redemption queue and exposure to their co-investors’ behaviour. The managed account answered that, from the allocator’s perspective.

That history matters because it tells you who has been driving this conversation, and it is not the managers.

Why this stopped being a niche

Unless you came from the FX and managed futures world, for most of its life the managed account was a structure for very large allocators writing very large tickets. That is no longer true, and the numbers are worth knowing because they will come up.

J.P. Morgan’s institutional investor survey found hedge fund SMA usage rose from 19% of investors in 2012 to 36% in 2018. Their 2018 manager benchmarking study found 56% of hedge fund managers already ran at least one SMA or fund of one. Managers between $1bn and $5bn averaged three of them. Above $5bn, nine. A large share of institutional hedge fund capital already moves this way.

The direction of travel has only sharpened since. BNP Paribas reported treasury efficiency as the single most cited reason allocators now use SMAs, with capital allocated this way growing materially over the last two years. AIMA, which published its first managed account guide in 2016 and an updated one in 2026, calls the current moment an SMA renaissance and points to prime-broker data showing managed accounts taking a rising share of new launches. IQ-EQ goes further and says nearly half of all new hedge fund launches now begin life as an SMA structure.

Two cautions on those figures. The forward projections, Goldman’s call for the space to grow by several hundred billion by 2027, J.P. Morgan’s estimate that most new launches will be SMAs, are forecasts cited second-hand, not realised data. And the “nearly half of launches” figures come from surveys run by the firms that service these structures, so treat them as directional rather than gospel. The cleanest hard numbers are the allocator surveys, and they all point the same way: this structure is moving from the edge to the centre.

So when an allocator raises a managed account, they are slotting you into a governance framework that a large part of the institutional market now runs by default.

What changes when you allocate through SMAs

If you sit on the allocator side, the managed account hands you control. It also hands you a pile of operational work you never had to think about inside a fund. The people running the most sophisticated platforms in the market are surprisingly candid about how much of this caught them off guard.

Start with the language. Allocators think in AUM. You write a $100 million ticket into a fund and everyone knows what that means. A managed account doesn’t work that way. You allocate in gross market value, long market value plus the absolute value of the shorts, and you set the GMV to land on the risk profile you want. In managed futures and FX you size in notional, and each notional can run at a different volatility, with different margin and collateral demands depending on the strategy. So which number is the ticket? How do you explain a $200 million GMV allocation, or a $100m notional at 10% vol, to an investment committee that has spent fifteen years thinking in fund AUM? Re-educating your own IC on how to even size the ticket is now part of the job.

Then the parts of the machine the fund used to run for you: financing and prime broker balances. In a managed account you own the unencumbered cash and you have to decide what to do with it. Do you sweep it, deploy it, take some risk with it? Should you move balances between counterparties? Do you even have the staff to action any of this? It becomes new operational territory.

And the relationship question underneath this. Once you are running meaningful size through a prime broker via managed accounts, you become a material client. Are you managing that relationship properly, so that you can extract the value you deserve from it: research, capital markets access, new issue allocations, the things prime brokers used to reserve for the largest pod shops in the world. Who owns that relationship with the prime brokers? You as the investor, the platform if you chose to operate an SMA through them, or the managers directing the flow?

One thing does get easier: operational due diligence. From the allocator’s perspective, a managed account can make for a far more streamlined ODD process. The allocator owns the structure, has autonomy over the service providers, and has full transparency over the portfolio. This means portfolio holdings, cash, leverage, risk limits and exposures can all be monitored directly. A lot of the traditional fund-level DD questions become less relevant when reviewing an SMA because the structure already answers them.

But the core operational risk still sits with the manager: governance, trade operations, compliance, technology, controls. Any operational DD still has to cover those in depth. The managed account removes a category of fund-level risk but it doesn’t make the manager risk-free.

This is where an allocation teaches you things a fund never will. In a fund you get month-end visibility and a number. In a managed account you watch the manager trade in real time, every day, through the drawdowns as well as the good runs. You see what they actually do against what they told you they do, which inside a fund is almost impossible to verify intra-month. And because most events don’t politely wait for month-end, you see how the manager handles the messy intra-month moment: the position that moves against them, the bad week. How they communicate under that pressure, how they behave when it isn’t going their way. You learn someone’s true colours fast. You will learn more about a manager in a few months in a managed account than in several years inside a fund.

The economics, and the financing edge nobody mentions

The headline most managers hear is that managed account fees run lower. I have personally seen SMA fees ranging from 1.5% and 15% to 0 and 15% and anything in between those two. The devil is always in the detail. I have seen structures with monthly, quarterly or yearly crystallisation of the performance fee, each yielding significantly different cash flow outcomes for the managers running them. I have also seen $50m managed account structures with 0 management fee and a $200k a year cost pass-through to cover systems. If you’re a manager, the fee is not the only number to pay attention to. Yet most of the managers I speak to are very focused on the fee alone.

And once you cut one deal, you have set a reference point. Grant a $50m account 0 and 15 with a cost pass-through and the next allocator will want to know why they are paying more. Most-favoured-nation clauses make that explicit and tie your hands on every account that follows. Before you agree generous terms to win the first ticket, work out what they commit you to across every ticket after it. The cheapest account you ever sign can quietly reprice the whole book.

For the allocator, the saving runs deeper than the management fee, and it is worth understanding even from the manager’s seat.

Inside a managed account a large institutional allocator implicitly borrows at around Fed funds plus 20 basis points through the structure. It is the cheapest funding available to them anywhere. If you used to allocate via external multi-managers, consider the impact of a second pass-through of performance fees and netting that a commingled multi-manager structure imposes, and the saving becomes explicit and calculable. One large US public fund modelled this for their board: Fixed costs, variable costs, financing terms, the leverage they would run, and the saving generated vs allocating via external multi-manager/pod funds. They put the annual number in the tens of millions of dollars, including reduced interest expense from running more capital-efficiently.

For smaller investors with different access to funding, the savings won’t be as large but just the cross-margining between different managers enabled by managed accounts will be a considerable saving.

That is what you are negotiating against. The allocator pushing for a managed account is capturing a financing and structural advantage that dwarfs the fee line. Understanding that changes the conversation from defending your headline rate to working out where the real value sits across the whole arrangement, including ticket size and the cost of serving the account.

It also gives you something to price against. If the allocator is capturing a financing and netting advantage worth multiples of your fee, that is a number you can point to when you negotiate ticket size and the cost pass-through. You are asking to share in a benefit the structure creates for them, and that is a reasonable thing to put on the table.

What changes when you sign one

As a manager, this is what actually changes when you start trading a managed account instead of a commingled fund. You run the same book. In almost every case the allocator just wants the strategy you already run, pari passu with your other capital. They are not asking you to do anything special. What changes is everything around the trading book.

Transparency becomes total. The investor sees what you buy and sell, daily, often close to real time. Your positioning, your sizing, your timing, the actual shape of how you trade, all of it is visible to a sophisticated observer. For a concentrated long/short book with a handful of large positions, or a systematic strategy whose logic can be reverse-engineered from enough position data over time, that visibility may carry a cost. Decide before you sign whether near-real-time transparency changes how you can run the strategy at all.

Your edge becomes a double-edged sword. One benefit of running on institutional infrastructure is that you have the same tools as everybody else. One drawback is that you have the same tools as everybody else. The same factor models, the same crowding signals. The same transparency that lets an allocator manage your risk also folds you into a pool where everyone can see whether the same edge is showing up across other managers at the same time.

Risk guidelines get agreed upfront, in writing, before you trade. Many managers underestimate this. Net and gross exposure, GMV, concentration limits, sector constraints, the drawdown you say you’d never expect to hit. It all goes in the investment management agreement before a single trade. In a good investor/manager relationship you set this collaboratively, but the risk guidelines are real and contractual. You can’t sell naked options if the IMA says so. You have termination clauses if your risk, intra month and not at month end, reaches certain limits, or if you deviate from your investment strategy.

Someone can hedge over the top of you. On the more advanced platforms there is a dynamic hedger that can take a position the allocator considers too large for your book and lay a targeted hedge against it to fit you inside their overall risk construct. You are still running your strategy, but you are running it inside a risk envelope that someone else is actively managing, with weekly risk calls covering credit, liquidity, factor exposure and the hedging overlay.

Allocation and best execution stop being your private business. Run the same book across a fund and three SMAs and you have to prove, not assert, that everyone is treated fairly. Who gets filled first, and how you evidence that no account is being favoured. This is the machinery that makes pari passu actually true rather than a word in a deck. Allocators ask about it and regulators expect it. A thin allocation policy looks fine until the day a fill is small and contested.

Your regulatory footprint can change. Taking on managed accounts can pull you into obligations you did not have running a single fund, depending on where you and the allocator sit: registration thresholds and the reporting regime you fall under. None of it is necessarily a problem. All of it is the kind of thing you want to know before you sign, not after a regulator asks.

You should agree, in advance, how you’d be fired. This is the cleanest and most adult part of the structure, and it surprises managers. In a great managed account relationship an exit playbook is agreed upfront. You sit down and agree a plan: the catalysts you’re playing for, and the level at which you’d walk. Usually the investor asks you directly what loss levels are expected and at what level they should terminate, and how that termination is triggered. You give them a level, and if you hit it you know what to expect. What most people hate in this industry is being surprised, and SMAs are built to reduce that risk. For a manager who trades well and communicates openly, that is a better deal than the traditional redemption cycle. For a manager who hopes to quietly trade through a bad patch, it is a far harder place to hide.

The redemption question, read from both sides

Managed accounts are often sold to managers as protection from redemption contagion, and that is partly true and partly a trap, so it is worth separating the two risks cleanly.

In a commingled fund you carry contagion risk. A large investor redeems, you sell positions to meet it, and in stressed conditions that can feed on itself across the whole book. Gates and suspensions exist, but using them damages your standing with every other investor at once.

In a managed account that contagion dynamic largely disappears. The allocator owns their assets in a segregated account. If they leave, their assets are dealt with on their own, without forcing sales that hit anyone else. An investor can just sweep the unencumbered cash in the account and walk away without disrupting anybody’s business, where in a fund this would have meant a redemption notice and a forced liquidation.

But you have swapped one risk for another. You now carry bilateral termination risk, and depending on the notice period you agreed, an allocator will likely be able to exit faster than a standard fund redemption cycle would allow. Contained, yes. Contagious, no. But the redemption cycle is potentially quicker and entirely in the allocator’s hands. The notice period is one of the most important numbers in the agreement and one of the most negotiable too.

And agree how the exit actually runs, not just when it can be triggered. When an allocator leaves, who liquidates the book and who wears the slippage of unwinding it. A clean-looking notice period means very little if the wind-down itself is left unspecified. For anything less than fully liquid, settle upfront how positions are valued and unwound on the way out, because that is the moment a tidy termination clause turns into an argument.

Platform or bespoke, and why it decides your operational life

The single biggest determinant of how painful a managed account is to run, and almost nobody distinguishes this clearly enough, is whether it sits on an established platform or is a bespoke bilateral arrangement.

On a platform, the infrastructure already exists. Reporting frameworks, custodian relationships, risk monitoring, onboarding. Some platforms described getting a manager up and trading in weeks, not months. You plug into an architecture rather than building one.

A bespoke bilateral account is a different animal. Each allocator brings their own preferences on custodian, reporting format, risk framework and operational review. Different service providers, different terms, all of it managed internally, by you.

The biggest risk for emerging managers taking on too many SMAs too early. Going from one SMA to two does not double the operational burden. It increases complexity exponentially, as every mandate is bespoke. A five-person team running a flagship fund and three separate SMAs simply does not have the operational resource to support them properly, and pretending otherwise is the place emerging managers most often come unstuck. The more customised the SMA, the more infrastructure, governance and people the structure quietly demands.

Underneath that sits the trap that gets managers into the mess in the first place. The pull of AUM is strong enough that emerging managers will say yes to almost any SMA opportunity in front of them. But it’s naive to think an SMA is just another LP allocation into the fund. Each one is a separate operating relationship with its own service providers, its own terms and its own ongoing demands on your team.

One account is manageable. Run three or four bespoke managed accounts for three or four allocators with different standards, on a lean operations team, and the cumulative load becomes the thing that breaks you. The question you should ask as an emerging manager is: can I run this specific account, on these specific terms, at a cost to serve that is proportionate to the size and the strategic value of this allocation.

The emerging manager’s real opportunity, and the catch underneath it

For emerging managers the upside is real. The managed account has largely replaced traditional seeding as the way new strategies get anchored. Combined with outsourced operations, it lets a talented PM launch lean, sometimes solo, with institutional-grade infrastructure from day one, even well below $100 million. For a manager with real ability and no franchise yet, that is the most accessible on-ramp to institutional capital that has ever existed. The ODD relief I mentioned earlier is precisely why an allocator will back you earlier than they otherwise would. That is real, and you should use it.

The catch is that the same structure that lets you launch lean also hands enormous leverage to whoever is on the other side. The isolated, no-contagion redemption that protects the allocator is, from your seat, the ability to pull your capital instantly and cleanly with no franchise-level cost to them. The total transparency that de-risks them erodes any informational edge you have. And there is no commingled base underneath you on which to build a franchise of your own, because the assets are theirs, not your fund’s.

Watch who is actually buying emerging-manager talent through these structures. Increasingly it is not end allocators. It is other funds and multi-manager platforms. BNP found that 9% of managers already allocate to their peers through external managed accounts, with a further 18% planning to. A growing share of the demand for your talent via managed account comes from platforms that will run you like a pod, except without the pod’s safety net or its commingled franchise. The structure that frees you can also quietly turn you into someone else’s book.

So go in with both eyes open and fight for the few terms that decide whether the structure works for you.

If there is a first-loss or seeding variant on the table, that calculus sharpens further. The one term that matters more than almost any other is whether you secure the rights to your own track record at the outset. Build a record inside someone else’s structure without that, and you can walk away with nothing portable to show for it.

And a reality check on size, because it bites emerging managers specifically. J.P. Morgan found the average minimum allocation to open an SMA or fund of one was around $73 million, with more than two-thirds of managers requiring at least $50 million. Below roughly $30 million an SMA rarely pays for itself, and for the structure to be viable longer term you really want $50 million or more.

That floor is strategy-dependent, though. For liquid trading strategies, FX, and managed futures or CTAs, where the operational load is lighter and the book is simpler to run, managed accounts work at far smaller sizes, often from $5 to $10 million. The $30 million number is really a guide for equity long/short and the more operationally heavy strategies, not a universal floor. Anything below that and the operational and expense drag quietly eats the relationship. For most equity and credit strategies it is an institutional-ticket structure, not a route for small-ticket capital. If the economics of serving the account don't work at the size on offer, the structure is not your friend regardless of how strategically flattering the request feels.

What to clarify before you sign, or before you allocate

Whichever side of the table you sit on, these are the points where ambiguity turns into trouble later. Get them explicit in the documentation rather than leaving them to assumption and goodwill.

Termination notice. The actual notice period for ending the mandate, and whether it is negotiable. This is your single most important defence against the speed of a bilateral exit. Read from the allocator side, it is your single most important source of control.

Information use. What the allocator can do with your position-level data. Can it be shared with advisers or consultants? Standard managed account documentation often leaves this unaddressed. Raise it regardless of how it gets resolved.

Investment guideline modification. Who can change the guidelines after the mandate starts, and on what timeline.

Trade allocation. How fills are allocated and averaged across this account and your other capital, and how fairness is evidenced. The thing nobody checks until a contested fill makes it matter.

Most-favoured-nation terms. Whether the fee and terms you agree here bind what you can offer, or refuse, every allocator after this one.

Reporting scope. What is required, how often, in what format, and how new reporting demands get handled later. Reporting obligations have a habit of expanding through the life of a relationship. Agree the framework for that expansion now.

Treatment of illiquid positions. If anything illiquid arises, how is it valued, and who governs the process between you and the allocator. This matters most for any strategy with exposure to less liquid situations, and it is the kind of thing nobody discusses until it is already a problem.

Tax and domicile. Because the investor owns the assets directly, the tax and withholding treatment can differ from a fund, especially across borders. Get it looked at before you sign, not at year end.

Regulatory impact. Whether taking this mandate changes your registration or reporting obligations.

Track record rights. Already flagged, repeated here because it is the one managers forget. If you are building a record inside this structure, secure the right to use it before you start.

Where this leaves you

The managed account is becoming the default wrapper for institutional hedge fund capital, and the trend is not reversing. For an emerging manager that is mostly good news. It is the most accessible on-ramp to serious capital that has existed in my time in this industry, and the stigma that used to attach to it has flipped into something close to a badge of seriousness.

But it is a structure designed, historically and operationally, around the needs of the person allocating, not the person managing. Almost everything published about it describes the benefits flowing one way. The fee saving you are offered is real, and smaller than the financing advantage sitting behind it. The transparency that wins you the allocation is the same transparency that erodes your edge, and the clean exit that makes the relationship adult is the same mechanism that lets your capital leave without warning. They are the terms to negotiate hard, because they decide whether you have signed an on-ramp or a cage.

If you are an emerging manager looking at a managed account request right now, forget whether managed accounts are good or bad. The real work is understanding what each specific arrangement asks of you operationally, and which terms you hold the line on. That is the conversation I have with managers before they sign. If you are in it now, you know where to find me.

One thing before you go. If you know a manager weighing their first managed account, or an allocator about to structure one, send them this. It is the piece I wish managers had in front of them before that first meeting, and it only reaches them if someone who has been on both sides passes it along. Forward it to the one person it would save from a bad term. Share it with anyone sitting at that table. That is the ask on this one.

Cláudia

P.S. If you have a managed account request on the table, or you're an allocator structuring one, this is the work I do. The terms that decide whether it works for you are the ones nobody sends over in advance. Email me and tell me which seat you're in. I answer every one.

This is very insightful. As an upcoming manager, this is really really helpful.

thank you for this article. I'm learning how to work with allocators and this is helpful